|

|

The chairman of the CFTC intimated last week before a Senate committee that some regulatory relief might be forthcoming. Meanwhile, a non-US cotton merchant was fined by the Commission for not filing required reports with the agency after self-reporting its own infractions and correcting its mistakes; and the adjudicatory arm of the Financial Industry Regulatory Authority recommended tougher sanctions for certain offenses. As a result, the following matters are covered in this week’s Bridging the Week:

Video Version:

Article Version:

CFTC Chairman Discloses Second Phase of Regulatory Review Before Senate Committee; Commissioner Giancarlo Questions Position Limits Proposal Before EnergyRisk Summit

Timothy Massad, Chairman of the Commodity Futures Trading Commission, disclosed last week before the US Senate Committee on Agriculture, Nutrition and Forestry that the CFTC has begun “step two” of a retrospective regulatory review to determine which CFTC rules “may need to be modified or rescinded.”

As part of this review, said Mr. Massad, the Commission will solicit public input and “follow-up with rulemaking proposals as necessary.” The Chairman provided no insight into the potential areas for rulemaking.

According to Mr. Massad, the CFTC’s reflective review is in response to Executive Order 13563 of President Obama (January 18, 2011). That order required agencies to

consider how best to promote retrospective analysis of rules that may be outmoded, ineffective, insufficient, or excessively burdensome, and to modify, streamline, expand, or repeal them in accordance with what has been learned.

(Click here to access Executive Order 13563.)

Mr. Massad said that the first phase of the CFTC’s retrospective review was its consideration of rules adopted in response to the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act. He claimed that, in response, the Commission modified a number of rules “to reflect market developments and to codify standard or commonly accepted industry practices.”

In his testimony, Mr. Massad also indicated that the Commission is looking at ways to improve its rules related to swap execution facilities. He indicated that, although SEF volumes “are growing,” and that one SEF already reports participation by 700 firms,

[w]e are looking at a number of additional issues concerning SEFs, such as the made available for trade determination process and concerns about the lack of post-trade anonymity for certain types of trades.

Mr. Massad acknowledged the input of Commissioner Giancarlo to the debate on SEFs, but rejected his proposal that “we should throw out the rules and start over.” However, he indicated that Mr. Giancarlo and he “had already found common ground on a number of changes that will improve the framework, and I expect that we will continue to do so.” (Click here for details of Mr. Giancarlo’s white paper of SEFs in the article, “CFTC Commissioner Laments Flawed US Swaps Trading Model” in the February 1, 2015 edition of Bridging the Week.)

Mr. Massad also noted the Commission is currently considering comments received in response to its September 2013 concept release on automated trading environments and is considering “what further steps may be necessary to further reduce risks in electronic and automated trading.” He provided no insight into a time frame for completion of this review other than "in the near future."

Separately, Commissioner J. Christopher Giancarlo severely criticized the CFTC’s proposed position limit rules before the EnergyRisk Summit in Houston, Texas.

In his presentation, Mr. Giancarlo argued that, because the run-up in oil prices prior to the 2008-2009 financial crisis “did not bear any of the signs of excessive speculation”, there is no evidence to support additional federal position limits in the energy markets. Indeed, because liquidity may be decreasing outside of the spot month, “the current problem [may not be] one of excessive speculation [but] of inadequate speculation.”

Mr. Giancarlo also criticized elements of the Commission’s proposal to eliminate storage transactions, merchandising and anticipatory hedging, cross-commodity hedges and gross versus net hedging from the categories of permissible hedges. According to Mr. Giancarlo,

I am very concerned that the overall effect of the CFTC’s bona fide hedging framework is to impose a federal regulatory edict in place of business judgment in the course of risk hedging activity by commercial enterprises. I believe that the CFTC must allow greater flexibility. It must encourage – not discourage – commercial enterprises to adapt to developments and advances in hedging practices.

Mr. Massad also told the Senate Committee that cybersecurity, information security and business continuity by clearinghouses, exchanges and SEFs represent a new challenge and risk to marketplaces that is being addressed by the CFTC. He said the CFTC currently requires clearinghouses and execution marketplaces to maintain adequate system safeguards and risk programs and to have recovery procedures; conducts system safeguard examinations to ensure exchanges’ and clearinghouses’ compliance with their requirements; and makes sure they conduct tests themselves of their cyber protections.

Briefly:

Compliance Weeds: The Cotton On-Call Report references part III of Form 304. It must be prepared by relevant cotton merchants and dealers as of the close of business each Friday and received in the CFTC’s New York office by no later than the second business day following the Friday date of the report. All persons holding or controlling reportable futures positions in cotton, any part of which are used for hedging fixed-price cash positions in cotton and cotton products are required to prepare a monthly report of their cash positions as of the close of business on the last Friday of each month on Parts I and II of Form 304, and received in the CFTC’s NY office no later than the second business day following the Friday date of the report. There is an equivalent CFTC report for persons who hold or control futures positions that are reportable in grains, soybeans, soybean oil and soybean meal, any part of which is a bona fide hedging position. This report – CFTC Form 204 – must also be prepared monthly as of close of business on the last Friday of each relevant month and received in the CFTC’s Chicago office by no later than the following third business day.

Compliance Weeds: Where there is a pre-trade communication to facilitate an IFUS futures or options trade on the exchange’s electronic trading system, both the buy and sell orders must be entered into the ETS and designated as a crossing order. At that point, a request for quote will be triggered for five seconds. Afterwards the trades may be crossed automatically by the ETS subject to various conditions. (Click here to access IFUS Rule 4.02(k) and here to access IFUS’s January 2015 Pre-Execution Communications FAQs.) Customers must always consent to their orders being shopped and the parties to pre-trade communications may not disclose the details of their communications to other parties. CME Group has some similar requirements and processes, although there are some important differences, and not all of its contracts available on Globex are eligible for pre-execution communications. (Click here to access CME Rule 539 and here to access CME Group MRAN RA1410-5 (December 15, 2014)). Pre-trade communication rules must be carefully reviewed exchange by exchange to ensure compliance. Crossing trades in violation of exchange rules potentially also violates the Commodity Futures Trading Commission’s prohibition against non-competitive trades. (Click here to access CFTC Rule 1.38(a).)

And even more briefly:

And finally:

Hard to Believe: It was Shakespeare’s Juliet who said, “[w]hat’s in a name? that which we call a rose/By any other name would smell as sweet.” However, the SEC’s and the Department of Justice’s cases against Sean and Robert Stewart allege that the father, Robert, also believed that a name is irrelevant. He thought that, by masquerading stock tips in golf colloquialisms, the advice would be fully understood no matter how camouflaged, claimed the regulators. Time will tell whether the SEC and the Department of Justice prevail in their allegations that an illicit stock tip is an illicit stock tip no matter what it’s called. And, separately, in another matter that occupied headlines last week, attorneys for New England Patriots quarterback Tom Brady argued it was unfair for their client to be suspended for four games because of his alleged “more probable than not” role in having footballs deflated to below minimum air pressure standards for a playoff game last year with the Indianapolis Colts. Counsel for the National Football League had previously claimed it was somewhat incriminating that one of the attendants who handled the suspect footballs had called himself Mr. Deflator. However, counsel for Mr. Brady claimed that the league’s attorney had entirely misinterpreted this reference. The attendant referred to himself as Mr. Deflator – not because he tampered with footballs – but because his goal was to lose weight; “deflate was a term … used to losing weight.” Perhaps for Juliet, a rose no matter the name would smell as sweet, but here something smells rotten – and it’s not “something rotten in the state of Denmark” (from Shakespeare’s tragedy Hamlet) but in Foxboro, Massachusetts! Time will tell on this matter too.

For more information, see:

FINRA Revises Sanction Guidelines for Misrepresentation and Fraud:

http://www.finra.org/sites/default/files/RegulatoryNotice_15-15.pdf

Cargill Fined US $300,000 by ICE Futures U.S. for Pre-Trade Communications; Two Related Firms Fined for Transferring Positions:

Cargill:

https://www.nfa.futures.org/basicnet/Case.aspx?entityid=0084857&case=2012-036&contrib=ICE

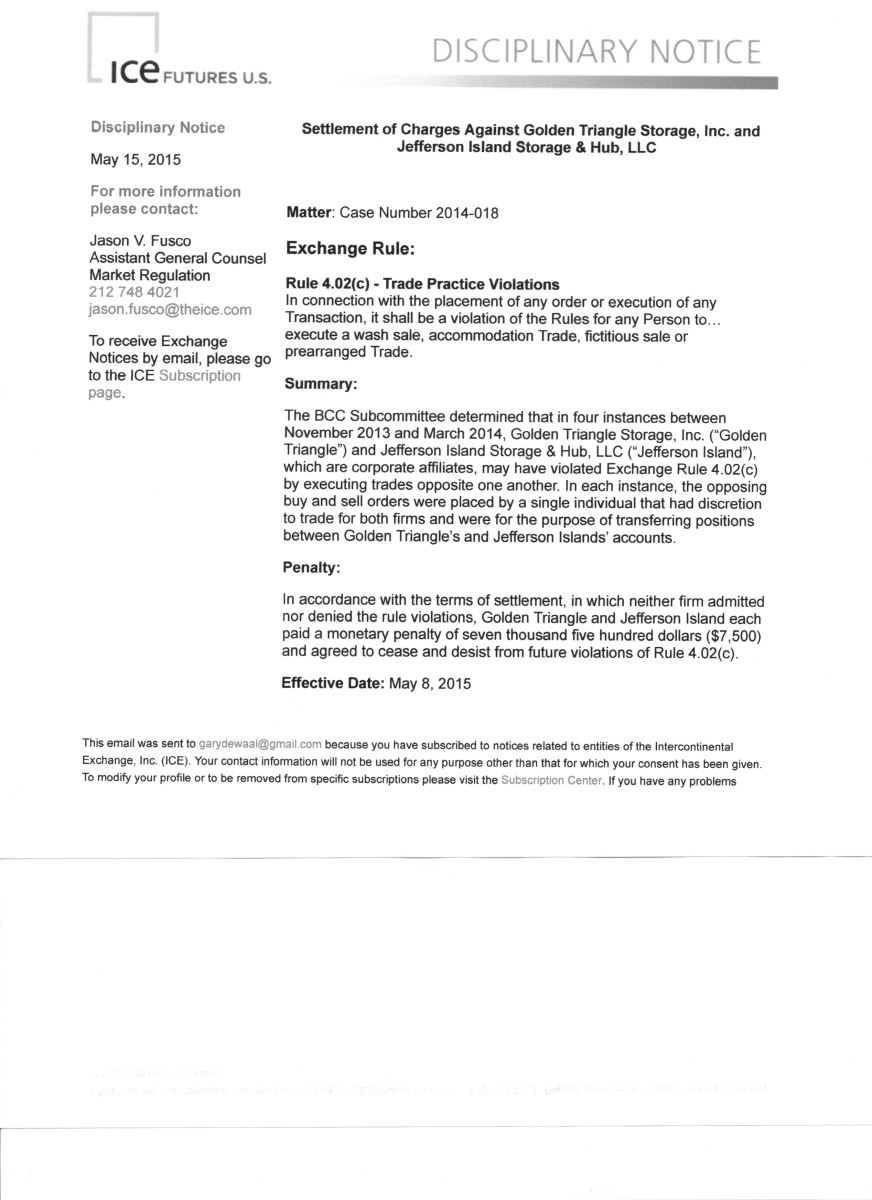

Golden Triangle Storage:

/ckfinder/userfiles/files/ICE%20Futures%20US%20Golden%20Triangle%20Storage.jpeg

CFTC Chairman Discloses Second Phase of Regulatory Review Before Senate Committee; Commissioner Giancarlo Questions Position Limits Proposal Before EnergyRisk Summit

Chairman Massad:

http://www.cftc.gov/PressRoom/SpeechesTestimony/opamassad-22

Commissioner Giancarlo:

http://www.cftc.gov/PressRoom/SpeechesTestimony/opagiancarlos-6

CFTC and SEC Clarify Status of Forward Contracts With Embedded Volumetric Optionality:

http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/federalregister051215.pdf

CME Group Combines All Block Trade Rules:

http://www.cmegroup.com/rulebook/files/mran-ra1506-5.pdf

Cyber Risk Poses Greater Risk to Broad Economy Than Geopolitical Events and New Regulations According to DTCC Survey:

http://dtcc.com/~/media/Files/pdfs/Systemic-Risk-Report-2015-Q1.pdf

ESMA Consults on Technical Standards for IRS Clearing:

http://www.esma.europa.eu/system/files/esma-2015-807_-_consultation_paper_no_4_on_the_clearing_obligation_irs_2.pdf

FINRA Files Enforcement Action Against Broker-Dealer, Chief Compliance Officer and Others for Unregistered Sales of Securities and Failure to Supervise:

http://disciplinaryactions.finra.org/Search/ViewDocument/48049

HK Intermediaries Reminded by SFC to Apply KYC AML Procedures: http://www.sfc.hk/edistributionWeb/gateway/EN/news-and-announcements/news/doc?refNo=15PR47

See also, SFC KYC Circular:

http://www.sfc.hk/edistributionWeb/gateway/EN/circular/openFile?refNo=15EC28

NASDAQ to Use Blockchain Technology to Enhance Equity Management Capabilities:

http://www.nasdaqomx.com/newsroom/pressreleases/pressrelease?messageId=1361706&displayLanguage=en

New Meaning for Old Words: When Golf References Are Allegedly Codes for Insider Trading, and Deflategate Is Allegedly Only About Weight Loss:

Deflategate:

http://wellsreportcontext.com

Department of Justice:

http://www.justice.gov/usao/nys/pressreleases/May15/StewartArrestPR/Stewart(s)%20Complaint.pdf

SEC:

http://www.sec.gov/litigation/complaints/2015/comp-pr2015-90.pdf

Non-US Cotton Merchant Fined US $480,000 for Not Filing Mandatory Weekly Reports of Physical Positions:

http://www.cftc.gov/ucm/groups/public/@lrenforcementactions/documents/legalpleading/enfliberoorder051115.pdf.pdf

The next edition of Bridging the Week will be published on June 1, 2015.

The information in this article is for informational purposes only and is derived from sources believed to be reliable as of May 16, 2015. No representation or warranty is made regarding the accuracy of any statement or information in this article. Also, the information in this article is not intended as a substitute for legal counsel, and is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. The impact of the law for any particular situation depends on a variety of factors; therefore, readers of this article should not act upon any information in the article without seeking professional legal counsel. Katten Muchin Rosenman LLP may represent one or more entities mentioned in this article. Quotations attributable to speeches are from published remarks and may not reflect statements actually made.

Gary DeWaal is currently Special Counsel with Katten Muchin Rosenman LLP in its New York office focusing on financial services regulatory matters. He provides advisory services and assists with investigations and litigation.

|

Social Media: |

May 03, 2020

April 12, 2020

March 29, 2020

Katten is a firm of first choice for clients seeking sophisticated, high-value legal services in the United States and abroad.

Our nationally recognized practices include corporate, financial services, litigation, real estate, environmental, commercial finance, insolvency and restructuring, intellectual property, and trusts and estates.

Our approximately 650 attorneys serve public and private companies, including nearly half of the Fortune 100, as well as a number of government and nonprofit organizations and individuals.

We provide full-service legal advice from locations across the United States and in London and Shanghai.

Gary DeWaal

Katten Muchin Rosenman LLP

575 Madison Avenue

New York, NY 10022-2585

+1.212.940.6558

{kind=link}

Bridging the Week by Gary DeWaal: May 11 to 15 and 18, 2015 (Retrospective Review, 304s, Pre-Trade Communications, Tougher Sanctions, Deflategate)

Jump to: AML and Bribery