|

|

Last week, the New York State Department of Financial Services enacted a requirement that all financial intermediaries engaging in a virtual currency business with a connection to New York State must first obtain a newly established BitLicense unless expressly exempted. In addition, the CFTC chairman provided insight into where the Commission may be headed in connection with its possible oversight of proprietary traders and algorithmic trading systems, while multiple respondents were fined for violations of Reg SHO, TRACE, position limits or non-disruptive trading requirements. Two firms, however, disputed CFTC allegations regarding their alleged manipulative conduct. As a result, the following matters are covered in this week’s Bridging the Week:

Video Version:

Article Version:

NYDFS Issues BitLicense Framework for Regulating Virtual Currency Firms

The New York State Department of Financial Services issued final regulations requiring a so-called “BitLicense” and establishing minimum standards for all financial intermediaries who engage in a virtual currency business activity from New York or to a NY resident.

The regulations impact a wide spectrum of potential businesses, although they exclude merchants and consumers who use virtual currencies in connection with transactions for goods or services, persons chartered under the NY banking law and approved to engage in a virtual currency business activity, and persons who engage in the mere “development and dissemination of software in and of itself.” This appears to exclude virtual currency miners, although the regulations are not entirely clear. According to Benjamin Lawsky, the departing superintendent for the NYDFS,

[S]tudents or other innovators who are simply developing software and are not holding onto customer funds are not required to apply for a BitLicense.

In general, the new regulations require all financial intermediaries engaging in a virtual currency business to apply and obtain a so-called BitLicense, and to maintain certain minimum standards and programs to help ensure customer protection, cybersecurity and anti-money laundering compliance.

Under the regulations, what constitutes a virtual currency should be broadly construed and includes any digital unit that is utilized as a medium of exchange or as a form of digitally stored value. However, virtual currencies do not include certain digital units that are used solely with online gaming platforms or as a part of a customer affinity or rewards program (with some restrictions), or that are used as part of prepaid cards.

Likewise, virtual currency business activity is broadly defined and includes (1) receiving virtual currency for transmission or transmitting virtual currency except where the transaction is for non-financial purposes and only involves a nominal amount; (2) storing or holding virtual currency for others; (3) buying and selling virtual currency as a customer business; (4) engaging as a customer business in the conversion or exchange of (a) fiat currency or other value into virtual currency, (b) virtual currency into fiat currency or other value, or (c) one form of virtual currency into another form of virtual currency; or (5) controlling, administering or issuing a virtual currency.

Applications for a BitLicense require extensive information about the applicant and its principals. Among the required information is a description of the firm’s proposed business activities, all relevant written policies and procedures, and fingerprints and a third-party prepared background report on each principal. Fingerprints and a photograph will also be required for each employee who may have access to customer funds.

Each virtual currency firm must have and enforce written compliance policies addressing anti-fraud, anti-money laundering, cybersecurity, privacy and information security. Virtual currency firms must maintain at all times “such capital in an amount and form as the superintendent determines is sufficient to ensure the financial integrity of the [l]icensee and its ongoing operations.”

Virtual currency firms are required to maintain and keep certain records in their original or native file format for at least seven years and submit themselves to examination by the NYDFS. They are also required to file quarterly unaudited financial statements and one annual financial statement that is certified. Such firms must appoint a chief compliance officer, a chief AML officer and a chief information security officer with specified responsibilities. Certain minimum risk disclosures are required to be made to all customers.

All virtual currency firms must apply for a license within 45 days of the unspecified effective date of the regulations or cease operating as a virtual currency firm. Material changes in business must be pre-approved by the NYDFS.

The NYDFS may grant perpetual licenses or two-year conditional licenses. All licenses can be revoked after a hearing upon a showing of “good cause.”

Nothing in the new NYDFS provisions regulates virtual currencies themselves.

(Click here for background on recent virtual currency regulatory developments in the November 13, 2014 advisory, "Recent Key Bitcoin and Virtual Currency Regulatory and Law Enforcement Developments" by Katten Muchin Rosenman LLP.)

My View: The NYDFS is the first US regulator to impose a specific requirement for virtual currency firms to obtain a BitLicense in order to conduct business and to require licensees to adhere to express minimum standards. It only can be hoped that other states contemplating regulations adopt equivalent requirements so interstate commerce involving virtual currency is not unnecessarily burdened. That being said, one thing that is particularly remarkable about the NYDFS BitLicense regulations are the requirements of licensees t0 maintain cybersecurity programs containing proscribed elements. In particular, the NYDFS expressly requires virtual currency firms to adhere to many of the best practices recommended (but not yet mandated) by other regulators, including identifying internal and external cyber risks, establishing procedures to protect the firm’s electronic systems and customer data, appointing a chief information security officer to oversee the firm’s cyber security program, requiring penetrating testing and audit trails, and requiring firms to maintain a business continuity and disaster recovery plan. Even financial service firms that are not involved in a virtual currency business should review these requirements to evaluate whether their own cybersecurity program would pass muster.

Briefly:

My View: In passing any new regulations, the Commission must continue to be mindful of the limitation of its resources. To the extent that tasks can be performed or already are performed by self-regulatory organizations, it appears more productive to heighten oversight of the SROs than to double-up on the requirements on market participants.

Hard to Believe: Reflecting on Commissioner Giancarlo’s 'Ode to FCMs' prompted me to recall that Shakespeare had also lamented about the state of futures commission merchants many years ago in an early draft of Hamlet’s famous soliloquy in Act 5, Scene 1, prior to amending it to its more customarily remembered version: “Alas poor FCMs, I knew them, Horatio; entities of seemingly infinite capacity, of most excellent clearing services. They hath carried our trades a thousand times; and now, how abhorred in my imagination it is! My gorge rises at it. Where are those firms we have transacted with now? Your names? Your logos? Your flashes of ingenuity that were wont to make our business folk buoyant? Not one now to assist in our clearinghouse access.” Of course, it is possible that I have Shakespeare confused with someone else.

Legal Weeds: Although there may be introducing brokers in connection with swaps activities, the CFTC’s IB rules do not neatly apply to swaps activities –particularly in connection with over-the-counter, non-cleared swaps. One CFTC rule – CFTC Rule 1.57 (click here to access) expressly sets forth requirements for all IBs, including that they must “[o]pen and carry each customer’s and option customer’s account with a carrying futures commission merchant” and transmit for execution all customer and option customer orders to a carrying FCM or a floor broker. These requirements, and others, make no sense in the context of OTC swaps. CFTC staff is applauded for deriving a common sense result in the circumstance of non-US persons handling swaps for international financial institutions located in the United States. However, the CFTC should reconsider its entire regulation of IBs to more appropriately align the current scope of IBs' authorized activities with an appropriate regulatory scheme.

And even more briefly:

And finally:

For more information, see:

Australian Futures Clearinghouse Applies for Exemption From DCO Registration:

http://www.cftc.gov/ucm/groups/public/@otherif/documents/ifdocs/asxclearfutdcoexemptpetition.pdf

CFTC Chairman Says Commission Considering Registration of Proprietary Traders With Direct Market Access; Commissioner Giancarlo Issues 'Ode to FCMs':

Giancarlo:

http://www.cftc.gov/PressRoom/SpeechesTestimony/giancarlostatement060115#SpTeMBL

Massad:

http://www.cftc.gov/PressRoom/SpeechesTestimony/opamassad-24

CFTC Grants Relief From IB and CTA Registration to Foreign Underwriters in Connection With Swap Activities of US-Based International Financial Institutions:

http://www.cftc.gov/ucm/groups/public/@lrlettergeneral/documents/letter/15-37.pdf

CFTC Stays ICE Futures U.S. Attempt to Increase Position Limits and Accountability Levels for Eight Financial Power Futures Contracts:

https://www.theice.com/publicdocs/futures_us/exchange_notices/ICE_Advisory_05_15_004_NYISO_Zone_G_PositionLimits_Stay.pdf

CME Group Requires Profit Disgorgement as Part of Position Limit Violation Settlements; Traders Settle for Alleged Spoofing-Type Conduct on Both CME Group and ICE Futures U.S.:

CME Group

Stephen Duggan:

http://www.cmegroup.com/tools-information/lookups/advisories/disciplinary/CBOT-12-9134-BC-STEPHEN-DUGGAN.html#pageNumber=1

Hayman Capital Management, LP:

http://www.cmegroup.com/tools-information/lookups/advisories/disciplinary/NYMEX-15-0071-BC-HAYMAN-CAPITAL-MANAGEMENT-LP.html#pageNumber=1

ICAP Corporates, LLC:

http://www.cmegroup.com/tools-information/lookups/advisories/disciplinary/NYMEX-12-8963-BC-ICAP-CORPORATES-LLC.html#pageNumber=1

Himanshu Kalra:

http://www.cmegroup.com/tools-information/lookups/advisories/disciplinary/COMEX-12-9004-BC-HIMANSHU-KALRA.html#pageNumber=1

Prosperity Steel United Singapore PTE Ltd.

http://www.cmegroup.com/tools-information/lookups/advisories/disciplinary/NYMEX-14-9758-BC-PROSPERITY-STEEL-UNITED-SINGAPORE-PTE-LTD.html#pageNumber=1

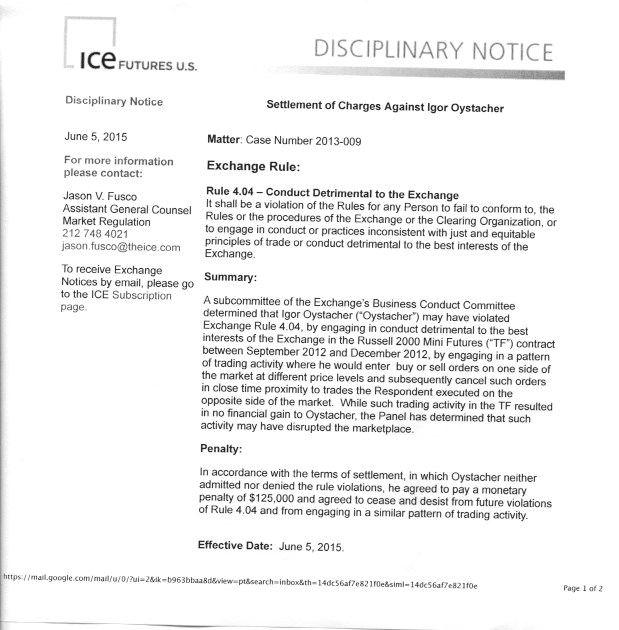

ICE Futures U.S.:

Igor Oystacher:

/ckfinder/userfiles/files/IFUS%20Oystacher.jpeg

DTCC Adds Its Voice to the Debate on CCP Default Loss Waterfalls:

http://www.dtcc.com/~/media/Files/Downloads/WhitePapers/CCP-Resiliency-Resources-White-Paper.pdf

FCA Seeks Views on Proposal to Require Non-Discriminatory Access to Regulated Benchmarks:

http://www.fca.org.uk/static/fca/documents/consultation-papers/cp15-18.pdf

EC Delays Implementation Date for Capital Hits to European Banks for Exposure to Non-Recognized Foreign Clearinghouses:

http://europa.eu/rapid/press-release_IP-15-5102_en.htm

Goldman Sachs Agrees to US $185,000 Fine With FINRA Related to Alleged TRACE Reporting Deficiencies:

http://disciplinaryactions.finra.org/Search/ViewDocument/54069

Joint Form of Financial Regulator Organizations Questions Whether Financial Firms Are Adequately Assessing Clearinghouse Risk:

http://www.bis.org/bcbs/publ/joint38.pdf

Kraft Foods and Mondelez Global Seek to Dismiss Parts of CFTC’s Manipulation Complaint:

https://www.law360.com/dockets/download/556cc574cd136f771c00016b?doc_url=https%3A%2F%2Fecf.ilnd.uscourts.gov%2Fdoc1%2F067115842695&label=Case+Filing

Leap Second is Coming June 30; Are You Ready?

CME Group:

http://www.cmegroup.com/company/files/leap-second-faq.pdf

LME:

https://www.lme.com/~/media/files/notices/2015/2015_06/15%20168%20a164%20-%20leap%20second%20impact%20and%20the%20lmeselect%20trading%20system%20-%20cancels%20and%20replaces%2015%20166%20a162%20docx.pdf

MAS Consults on Regulatory Framework for Intermediaries Dealing in OTC Derivatives:

http://www.mas.gov.sg/~/media/MAS/News%20and%20Publications/Consultation%20Papers/Policy%20Consultation%20on%20Regulatory%20Framework%20for%20OTC%20Intermediaries%20ERA%20and%20Marketing%20of%20CIS%203%20Jun%2015.pdf

Merrill Lynch Agrees to US $11 Million Payment to Resolve SEC Short Sale Charges:

http://www.sec.gov/litigation/admin/2015/34-75083.pdf

NYDFS Issues BitLicense Framework for Regulating Virtual Currency Firms:

Overview of Benjamin Lawsky:

http://www.dfs.ny.gov/about/speeches/sp1506031.htm

Regulation:

http://www.dfs.ny.gov/legal/regulations/adoptions/dfsp200t.pdf

OFAC Removes Certain Cuba Nationals From SDN List:

http://www.treasury.gov/resource-center/sanctions/OFAC-Enforcement/Pages/20150604.aspx

The information in this article is for informational purposes only and is derived from sources believed to be reliable as of June 6, 2015. No representation or warranty is made regarding the accuracy of any statement or information in this article. Also, the information in this article is not intended as a substitute for legal counsel, and is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. The impact of the law for any particular situation depends on a variety of factors; therefore, readers of this article should not act upon any information in the article without seeking professional legal counsel. Katten Muchin Rosenman LLP (Katten) may represent one or more entities mentioned in this article. Quotations attributable to speeches are from published remarks and may not reflect statements actually made. Views expressed by the author are not necessarily the views of Katten or any of its directors or officers.

Gary DeWaal is currently Special Counsel with Katten Muchin Rosenman LLP in its New York office focusing on financial services regulatory matters. He provides advisory services and assists with investigations and litigation.

|

Social Media: |

May 03, 2020

April 12, 2020

March 29, 2020

Katten is a firm of first choice for clients seeking sophisticated, high-value legal services in the United States and abroad.

Our nationally recognized practices include corporate, financial services, litigation, real estate, environmental, commercial finance, insolvency and restructuring, intellectual property, and trusts and estates.

Our approximately 650 attorneys serve public and private companies, including nearly half of the Fortune 100, as well as a number of government and nonprofit organizations and individuals.

We provide full-service legal advice from locations across the United States and in London and Shanghai.

Gary DeWaal

Katten Muchin Rosenman LLP

575 Madison Avenue

New York, NY 10022-2585

+1.212.940.6558

{kind=link}

Bridging the Week by Gary DeWaal: June 1 to 5 and 8, 2015 (BitLicense, Reg SHO, TRACE, CCPs, Manipulation and Shakespeare)

Jump to: AML and Bribery