Bridging the Week by Gary DeWaal

The chairman of the CFTC intimated last week before a Senate committee that some regulatory relief might be forthcoming. Meanwhile, a non-US cotton merchant was fined by the Commission for not filing required reports with the agency after self-reporting its own infractions and correcting its mistakes; and the adjudicatory arm of the Financial Industry Regulatory Authority recommended tougher sanctions for certain offenses. As a result, the following matters are covered in this week’s Bridging the Week:

- CFTC Chairman Discloses Second Phase of Regulatory Review Before Senate Committee; Commissioner Giancarlo Questions Position Limits Proposal Before EnergyRisk Summit;

- Non-US Cotton Merchant Fined US $480,000 for Not Filing Mandatory Weekly Reports of Physical Positions (includes Compliance Weeds);

- Cargill Fined US $300,000 by ICE Futures U.S. for Pre-Trade Communications; Two Related Firms Fined for Transferring Positions (includes Compliance Weeds);

- FINRA Files Enforcement Action Against Broker-Dealer, Chief Compliance Officer and Others for Unregistered Sales of Securities and Failure to Supervise;

- New Meaning for Old Words: When Golf References Are Allegedly Codes for Insider Trading, and Deflategate Is Allegedly Only About Weight Loss (includes Hard to Believe); and more.

Video Version:

Article Version:

CFTC Chairman Discloses Second Phase of Regulatory Review Before Senate Committee; Commissioner Giancarlo Questions Position Limits Proposal Before EnergyRisk Summit

Timothy Massad, Chairman of the Commodity Futures Trading Commission, disclosed last week before the US Senate Committee on Agriculture, Nutrition and Forestry that the CFTC has begun “step two” of a retrospective regulatory review to determine which CFTC rules “may need to be modified or rescinded.”

As part of this review, said Mr. Massad, the Commission will solicit public input and “follow-up with rulemaking proposals as necessary.” The Chairman provided no insight into the potential areas for rulemaking.

According to Mr. Massad, the CFTC’s reflective review is in response to Executive Order 13563 of President Obama (January 18, 2011). That order required agencies to

consider how best to promote retrospective analysis of rules that may be outmoded, ineffective, insufficient, or excessively burdensome, and to modify, streamline, expand, or repeal them in accordance with what has been learned.

(Click here to access Executive Order 13563.)

Mr. Massad said that the first phase of the CFTC’s retrospective review was its consideration of rules adopted in response to the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act. He claimed that, in response, the Commission modified a number of rules “to reflect market developments and to codify standard or commonly accepted industry practices.”

In his testimony, Mr. Massad also indicated that the Commission is looking at ways to improve its rules related to swap execution facilities. He indicated that, although SEF volumes “are growing,” and that one SEF already reports participation by 700 firms,

[w]e are looking at a number of additional issues concerning SEFs, such as the made available for trade determination process and concerns about the lack of post-trade anonymity for certain types of trades.

Mr. Massad acknowledged the input of Commissioner Giancarlo to the debate on SEFs, but rejected his proposal that “we should throw out the rules and start over.” However, he indicated that Mr. Giancarlo and he “had already found common ground on a number of changes that will improve the framework, and I expect that we will continue to do so.” (Click here for details of Mr. Giancarlo’s white paper of SEFs in the article, “CFTC Commissioner Laments Flawed US Swaps Trading Model” in the February 1, 2015 edition of Bridging the Week.)

Mr. Massad also noted the Commission is currently considering comments received in response to its September 2013 concept release on automated trading environments and is considering “what further steps may be necessary to further reduce risks in electronic and automated trading.” He provided no insight into a time frame for completion of this review other than "in the near future."

Separately, Commissioner J. Christopher Giancarlo severely criticized the CFTC’s proposed position limit rules before the EnergyRisk Summit in Houston, Texas.

In his presentation, Mr. Giancarlo argued that, because the run-up in oil prices prior to the 2008-2009 financial crisis “did not bear any of the signs of excessive speculation”, there is no evidence to support additional federal position limits in the energy markets. Indeed, because liquidity may be decreasing outside of the spot month, “the current problem [may not be] one of excessive speculation [but] of inadequate speculation.”

Mr. Giancarlo also criticized elements of the Commission’s proposal to eliminate storage transactions, merchandising and anticipatory hedging, cross-commodity hedges and gross versus net hedging from the categories of permissible hedges. According to Mr. Giancarlo,

I am very concerned that the overall effect of the CFTC’s bona fide hedging framework is to impose a federal regulatory edict in place of business judgment in the course of risk hedging activity by commercial enterprises. I believe that the CFTC must allow greater flexibility. It must encourage – not discourage – commercial enterprises to adapt to developments and advances in hedging practices.

Mr. Massad also told the Senate Committee that cybersecurity, information security and business continuity by clearinghouses, exchanges and SEFs represent a new challenge and risk to marketplaces that is being addressed by the CFTC. He said the CFTC currently requires clearinghouses and execution marketplaces to maintain adequate system safeguards and risk programs and to have recovery procedures; conducts system safeguard examinations to ensure exchanges’ and clearinghouses’ compliance with their requirements; and makes sure they conduct tests themselves of their cyber protections.

Briefly:

- Non-US Cotton Merchant Fined $480,000 for Not Filing Mandatory Weekly Reports of Physical Positions: Libero Commodities S.A., a non-US-based agricultural trading company, agreed to pay a fine of US $480,000 to the Commodity Futures Trading Commission for not filing mandatory weekly reports of its cotton purchases and sales since it began trading in May 2010 through April 29, 2014. Under CFTC rules, all cotton merchants and dealers, wherever located, who hold or control cotton futures positions in excess of reportable levels (e.g., 100 contracts for cotton) are required to file with the CFTC a Form 304 on a weekly basis setting forth all cotton bought or sold, or contracted for purchase or sale, at a price to be fixed later, referencing the relevant ICE Futures U.S. futures contract month on which the price is based (or if the reference is other than an ICE Futures U.S. contract month). According to the CFTC, on over 200 occasions during the relevant period, Libero failed to file with the CFTC a required Form 304. Libero, which is principally based in Geneva, Switzerland and maintains an office in Mato Grasso, Brazil, self-reported its violations, said the CFTC. In accepting Libero’s offer of settlement, the CFTC acknowledged Libero”s “cooperation in this matter, which included proactively and voluntarily analyzing its past trading activity since its inception and retroactively compiling and providing all of the back CFTC Form 304[s] that should have been filed with the Commission.” Last year, the CFTC fined two subsidiaries of Mitsui Corp US $500,000 for their failure to file mandatory weekly cotton reports. (Click here to access details in the article, "CFTC Fines Cotton Traders for Not Filing Weekly Reports Showing Their Physical Purchases and Sales" in the January 20, 2014 edition of Bridging the Week.)

Compliance Weeds: The Cotton On-Call Report references part III of Form 304. It must be prepared by relevant cotton merchants and dealers as of the close of business each Friday and received in the CFTC’s New York office by no later than the second business day following the Friday date of the report. All persons holding or controlling reportable futures positions in cotton, any part of which are used for hedging fixed-price cash positions in cotton and cotton products are required to prepare a monthly report of their cash positions as of the close of business on the last Friday of each month on Parts I and II of Form 304, and received in the CFTC’s NY office no later than the second business day following the Friday date of the report. There is an equivalent CFTC report for persons who hold or control futures positions that are reportable in grains, soybeans, soybean oil and soybean meal, any part of which is a bona fide hedging position. This report – CFTC Form 204 – must also be prepared monthly as of close of business on the last Friday of each relevant month and received in the CFTC’s Chicago office by no later than the following third business day.

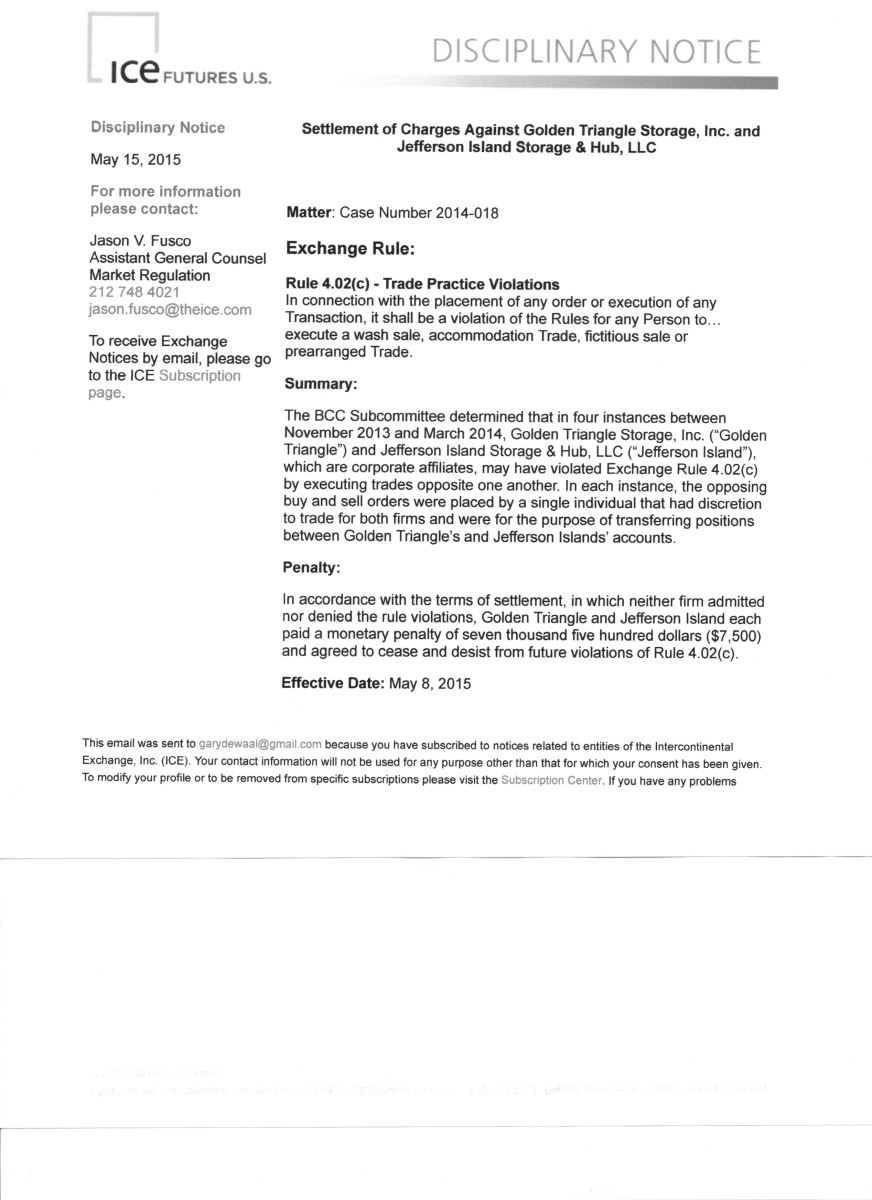

- Cargill Fined US $300,000 by ICE Futures U.S. for Pre-Trade Communications; Two Related Firms Fined for Transferring Positions: Cargill Incorporated agreed to settle a disciplinary action brought by ICE Futures U.S. related to its alleged failure to expose multiple futures orders to the market for at least five seconds prior to crossing them on the exchange’s electronic trading system against other orders following pre-trade communications. This requirement existed under a predecessor to IFUS’s current rule dealing with crossing trades (click here to access now withdrawn ICE Futures Rule 27.22). To settle this matter, Cargill agreed to pay a fine of US $300,000 and to comply with IFUS’s pre-execution communication procedures going forward. Separately, Golden Triangle Storage & Hub LLC and Jefferson Island Storage & Hub LLC each agreed to pay a fine of US $7,500 to IFUS in connection with buy and sell orders placed by a single person with discretion to trade for both firms for the alleged purpose of transferring positions from one firm to the other.

Compliance Weeds: Where there is a pre-trade communication to facilitate an IFUS futures or options trade on the exchange’s electronic trading system, both the buy and sell orders must be entered into the ETS and designated as a crossing order. At that point, a request for quote will be triggered for five seconds. Afterwards the trades may be crossed automatically by the ETS subject to various conditions. (Click here to access IFUS Rule 4.02(k) and here to access IFUS’s January 2015 Pre-Execution Communications FAQs.) Customers must always consent to their orders being shopped and the parties to pre-trade communications may not disclose the details of their communications to other parties. CME Group has some similar requirements and processes, although there are some important differences, and not all of its contracts available on Globex are eligible for pre-execution communications. (Click here to access CME Rule 539 and here to access CME Group MRAN RA1410-5 (December 15, 2014)). Pre-trade communication rules must be carefully reviewed exchange by exchange to ensure compliance. Crossing trades in violation of exchange rules potentially also violates the Commodity Futures Trading Commission’s prohibition against non-competitive trades. (Click here to access CFTC Rule 1.38(a).)

- FINRA Files Enforcement Action Against Broker-Dealer, Chief Compliance Officer and Others for Unregistered Sales of Securities and Failure to Supervise: The Financial Industry Regulatory Authority filed an administrative complaint against Scottsdale Capital Advisors Corporation, a registered broker-dealer and FINRA member, for the alleged sale of 74 million shares of unregistered microcap stocks of three US-incorporated companies from December 1, 2013, through June 30, 2014. In its complaint, FINRA also named D. Michael Cruz, Scottsdale’s president; Timothy DiBlasi, its chief compliance officer; and John Hurry, a director. FINRA claimed that Mr. Hurry indirectly owned Scottsdale, as well as Alpine Securities Corporation, Scottsdale’s clearing firm. According to FINRA, Mr. Hurry deposited the shares into accounts and subaccounts at Scottsdale in the name of CSCT, which he owned and controlled. FINRA claimed that Mr. Hurry used the three firms he allegedly controlled – CSCT, Scottsdale and Alpine – to facilitate the microcap liquidations “without the scrutiny that the transactions demanded.” FINRA claimed all the liquidations followed a similar pattern: a third party first loaned funds to the issuer of the microcap stock. This loan ultimately was converted to stock shares by a foreign corporate customer of another foreign corporate customer of CSCT. CSCT would then deposit the shares – typically in certificate form — into an account at Scottsdale for the customer of its customer, and then shortly afterwards, liquidate the shares and wire the funds out. None of the shares were registered with the Securities and Exchange Commission or exempt from registration, as required, claimed FINRA. FINRA claimed that Mr. DiBlasi was responsible for implementing and ensuring that all stock certificates were validly issued and owned by its customers, and that resales were made in reliance on an exemption from registration requirements in order to prevent the sale of unregistered non-exempt stocks. He was charged for allegedly failing to fulfill his obligations in connection with the relevant microcap liquidations. FINRA alleged that clients of Scottsdale realized in excess of US $1.7 million as a result of the illicit trading. In November 2011, Scottsdale consented to a fine by FINRA of US $125,000 related to its alleged sale of unregistered securities and not maintaining an adequate anti-money laundering program. In the new complaint, FINRA seeks findings of rule violations and disgorgement of all profits against the respondents, among other sanctions.

And even more briefly:

- CME Group Combines All Block Trade Rules: The CME Group proposed a common single rule for block trades for all its four exchanges. The current rules differ slightly among the exchanges by providing different times for block trade reporting. The new single rule says that block trades must be reported “within the time period and in the manner specified by the Exchange.” In addition, CME Group proposes to have a single interpretive guidance regarding block trades for all four of its exchanges, instead of one for the Commodity Exchange, Inc. and New York Mercantile Exchange, and a separate one for the Chicago Mercantile Exchange and the Chicago Board of Trade. The new guidance will highlight in a single document differences among the CME Group exchanges regarding block trade minimum quantities, reporting requirements and price reporting methods. The new rule and guidance are proposed to be effective May 29, 2015.

- NASDAQ to Use Blockchain Technology to Enhance Equity Management Capabilities: NASDAQ announced that, later this year, it will employ blockchain technology to enhance the equity management capabilities offered by its private market platform. Most famously, a “blockchain” refers to the public ledger on which all Bitcoin transactions are recorded. According to NASDAQ, “the creation of a securities distributed ledger function using blockchain technology will provide extensive integrity, audit ability, governance and transfer of ownership capabilities.” The head of this initiative for NASDAQ, Fredrik Voss, has been given the title "Blockchain Technology Evangelist." (Click here for an introduction to Bitcoin and an overview of relevant regulatory developments in the November 26, 2013 article “Bitcoin: Current US Regulatory Developments” by Katten Muchin Rosenman.)

- FINRA Revises Sanction Guidelines for Misrepresentation and Fraud: The National Adjudicatory Council, the appellate tribunal for disciplinary cases of the Financial Industry Regulatory Authority, has increased the severity of potential sanctions FINRA adjudicators should consider for members who have been found to have engaged in misrepresentations or violated FINRA’s suitability requirements. Among other matters, adjudicators should now “strongly consider” barring an individual where there has been a finding of fraud, misrepresentation or material omissions of fact, rather than solely “considering” a bar, absent mitigating factors. Likewise, for intentional or reckless fraud by a firm, an adjudicator should now “strongly consider” expelling a firm from FINRA membership “where aggravating factors predominate the firm’s misconduct.” An individual should be suspended from 31 calendar days to two years for negligent misrepresentations or material omissions of fact, says NAC. In general, NAC recommends that sanctions in disciplinary cases “should be significant enough to achieve deterrence, and not a mere cost of doing business.” (Click here for additional details in the article, “FINRA’s NAC Strengthens Sanction Guidelines Related to Fraud and Suitability” in the May 15, 2015 edition of Corporate & Financial Weekly Digest by Katten Muchin Rosenman LLP.)

- CFTC and SEC Clarify Status of Forward Contracts With Embedded Volumetric Optionality: The Commodity Futures Trading Commission and the Securities and Exchange Commission jointly issued a CFTC interpretation of when an agreement, contract or transaction with volumetric optionality will constitute a forwards contract as opposed to a swaps contract. According to the interpretation, this will be the case when an arrangement relating to a non-financial commodity satisfies seven standards, including that it is between commercial parties; the embedded optionality does not undermine the overall nature of arrangement as a forward contract; the predominant characteristic of the arrangement is delivery; the embedded optionality cannot be separated and marketed separately from the overall transaction; and the volumetric optionality is meant to address “physical or regulatory requirements that reasonably influence demand for, or supply of, the nonfinancial commodity," among other standards. (Click here for additional details in the article, “CFTC Revises Interpretation on Forward Contracts with Embedded Volumetric Optionality” in the May 15, 2015 edition of Corporate & Financial Weekly Digest by Katten Muchin Rosenman LLP.)

- Cyber Risk Poses Greater Risk to Broad Economy Than Geopolitical Events and New Regulations According to DTCC Survey: The Depository Trust & Clearing Corporation issued a survey of its members conducted during the first quarter of 2015 that indicated that cyber risk was the greatest concern – outflanking concern about geopolitical risk and the impact of new regulations. Forty-six percent of respondents voted cyber threats as their greatest concern, as opposed to thirty-three percent in September 2014. Earlier this year, both the Office of Compliance Inspections and Examinations and the Financial Industry Regulatory Authority published observations from their review of cybersecurity practices at securities industry firms — on both the buy and sell sides. FINRA also identified principles and effective practices firms should consider to address cybersecurity threats. (Click here for details in the article, “Industry Watchdogs Warn Brokers and Advisory Firms on Cybersecurity Threats” in the February 8, 2015 edition of Bridging the Week.) More recently, the SEC's Division of Investment Management also issued guidance to registered investment companies and advisers regarding cybersecurity. (Click here for details in the article, "SEC's Division of Investment Management Provides tips to Enhance Cybersecurity at Investment Companies and Advisers" in the May 3, 2015 edition of Bridging the Week.)

- ESMA Consults on Technical Standards for IRS Clearing: The European Securities and Markets Authority has issued a consultation paper seeking input on proposed regulatory technical standards for establishing a clearing obligation for additional classes of interest rate swaps that were not included in a prior RTS for IRS clearing obligations. The additional classes of IRS are fixed-to-float IRSs denominated in Czech Koruna, Danish Krone, Hungarian Forint, Norwegian Krone (NOK), Swedish Krona (SEK) and Polish Zloty (PLN) and forward rate agreements denominated in NOK, SEK and PLN. Comments will be accepted by ESMA through July 15.

- HK Intermediaries Reminded by SFC to Apply KYC AML Procedures: The Hong Kong Securities and Futures Commission reminded intermediaries of the need to follow appropriate account opening procedures to abide by know your client requirements for investors in and outside of HK. The SFC issued revised guidance after it identified “deficiencies and unsatisfactory practices” during reviews of firms’ KYC and account opening procedures. The circular particularly discourages firms from relying on non-financial affiliates to perform required KYC certifications.

And finally:

- New Meaning for Old Words: When Golf References Are Allegedly Codes for Insider Trading, and Deflategate Is Allegedly Only About Weight Loss: The Securities and Exchange Commission filed civil insider-trading charges against Sean Stewart and his father, Robert Stewart, in a federal court in New York. Federal criminal charges were filed simultaneously against the father and son in the same federal court by the US Attorney’s office located in Manhattan. The SEC alleged that, on at least six occasions from 2010 to 2014, the son provided trading tips to his father on future mergers and acquisitions in breach of duties he owed his investment bank employers and the companies they advised (the son worked at two different investment banks during the relevant time). According to the SEC, the father used an unnamed third person, a friend, to place the relevant trades based on the inside information. The father and his friend together made approximately US $1.1 million as a result of these transactions, said the SEC. Some of this money was kicked back to the son, including as payment for part of his son’s wedding expenses, claimed the SEC. Among other techniques to avoid detection, charged the SEC, the father and his friends met primarily in person to discuss the illicit transactions and used coded email messages referencing golf to help disguise their trading. For example, to alert his friend to purchase options in one company his son specified, the father wrote to his friend that he “might have an opportunity to play golf – but would need to book the reservation as soon as the office opens Tuesday morning.” Based on this coded advice and prior information the father shared with him, the friend purchased options in the relevant company on the next Tuesday morning, the SEC charged. The SEC seeks disgorgement of profits and civil penalties against the respondents. The respondents were charged criminally with multiple counts of conspiracy to commit wire fraud, securities fraud and fraud in connection with a tender offer. Each charge could result in a maximum prison term of 20 years for each respondent.

Hard to Believe: It was Shakespeare’s Juliet who said, “[w]hat’s in a name? that which we call a rose/By any other name would smell as sweet.” However, the SEC’s and the Department of Justice’s cases against Sean and Robert Stewart allege that the father, Robert, also believed that a name is irrelevant. He thought that, by masquerading stock tips in golf colloquialisms, the advice would be fully understood no matter how camouflaged, claimed the regulators. Time will tell whether the SEC and the Department of Justice prevail in their allegations that an illicit stock tip is an illicit stock tip no matter what it’s called. And, separately, in another matter that occupied headlines last week, attorneys for New England Patriots quarterback Tom Brady argued it was unfair for their client to be suspended for four games because of his alleged “more probable than not” role in having footballs deflated to below minimum air pressure standards for a playoff game last year with the Indianapolis Colts. Counsel for the National Football League had previously claimed it was somewhat incriminating that one of the attendants who handled the suspect footballs had called himself Mr. Deflator. However, counsel for Mr. Brady claimed that the league’s attorney had entirely misinterpreted this reference. The attendant referred to himself as Mr. Deflator – not because he tampered with footballs – but because his goal was to lose weight; “deflate was a term … used to losing weight.” Perhaps for Juliet, a rose no matter the name would smell as sweet, but here something smells rotten – and it’s not “something rotten in the state of Denmark” (from Shakespeare’s tragedy Hamlet) but in Foxboro, Massachusetts! Time will tell on this matter too.

For more information, see:

FINRA Revises Sanction Guidelines for Misrepresentation and Fraud:

http://www.finra.org/sites/default/files/RegulatoryNotice_15-15.pdf

Cargill Fined US $300,000 by ICE Futures U.S. for Pre-Trade Communications; Two Related Firms Fined for Transferring Positions:

Cargill:

https://www.nfa.futures.org/basicnet/Case.aspx?entityid=0084857&case=2012-036&contrib=ICE

Golden Triangle Storage:

/ckfinder/userfiles/files/ICE%20Futures%20US%20Golden%20Triangle%20Storage.jpeg

CFTC Chairman Discloses Second Phase of Regulatory Review Before Senate Committee; Commissioner Giancarlo Questions Position Limits Proposal Before EnergyRisk Summit

{kind=link}

Chairman Massad:

http://www.cftc.gov/PressRoom/SpeechesTestimony/opamassad-22

Commissioner Giancarlo:

http://www.cftc.gov/PressRoom/SpeechesTestimony/opagiancarlos-6

CFTC and SEC Clarify Status of Forward Contracts With Embedded Volumetric Optionality:

http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/federalregister051215.pdf

CME Group Combines All Block Trade Rules:

http://www.cmegroup.com/rulebook/files/mran-ra1506-5.pdf

Cyber Risk Poses Greater Risk to Broad Economy Than Geopolitical Events and New Regulations According to DTCC Survey:

http://dtcc.com/~/media/Files/pdfs/Systemic-Risk-Report-2015-Q1.pdf

ESMA Consults on Technical Standards for IRS Clearing:

http://www.esma.europa.eu/system/files/esma-2015-807_-_consultation_paper_no_4_on_the_clearing_obligation_irs_2.pdf

FINRA Files Enforcement Action Against Broker-Dealer, Chief Compliance Officer and Others for Unregistered Sales of Securities and Failure to Supervise:

http://disciplinaryactions.finra.org/Search/ViewDocument/48049

HK Intermediaries Reminded by SFC to Apply KYC AML Procedures: http://www.sfc.hk/edistributionWeb/gateway/EN/news-and-announcements/news/doc?refNo=15PR47

See also, SFC KYC Circular:

http://www.sfc.hk/edistributionWeb/gateway/EN/circular/openFile?refNo=15EC28

NASDAQ to Use Blockchain Technology to Enhance Equity Management Capabilities:

http://www.nasdaqomx.com/newsroom/pressreleases/pressrelease?messageId=1361706&displayLanguage=en

New Meaning for Old Words: When Golf References Are Allegedly Codes for Insider Trading, and Deflategate Is Allegedly Only About Weight Loss:

Deflategate:

http://wellsreportcontext.com

Department of Justice:

http://www.justice.gov/usao/nys/pressreleases/May15/StewartArrestPR/Stewart(s)%20Complaint.pdf

SEC:

http://www.sec.gov/litigation/complaints/2015/comp-pr2015-90.pdf

Non-US Cotton Merchant Fined US $480,000 for Not Filing Mandatory Weekly Reports of Physical Positions:

http://www.cftc.gov/ucm/groups/public/@lrenforcementactions/documents/legalpleading/enfliberoorder051115.pdf.pdf

The next edition of Bridging the Week will be published on June 1, 2015.

The information in this article is for informational purposes only and is derived from sources believed to be reliable as of May 16, 2015. No representation or warranty is made regarding the accuracy of any statement or information in this article. Also, the information in this article is not intended as a substitute for legal counsel, and is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. The impact of the law for any particular situation depends on a variety of factors; therefore, readers of this article should not act upon any information in the article without seeking professional legal counsel. Katten Muchin Rosenman LLP may represent one or more entities mentioned in this article. Quotations attributable to speeches are from published remarks and may not reflect statements actually made.

© 2024 Katten Muchin Rosenman and Gary DeWaal. All Rights Reserved.

Bridging the Week by Gary DeWaal: May 11 to 15 and 18, 2015 (Retrospective Review, 304s, Pre-Trade Communications, Tougher Sanctions, Deflategate)

AML and Bribery Bitcoin Ecosystem Bridging the Week Chief Compliance Officers Compliance Weeds Cybersecurity Hard to Believe Position and Trade Reporting Trade Practices (including Disruptive Trading) Uncleared Swaps