|

|

A bit of new and a bit of old highlighted international financial regulatory developments this past week. The Commodity Futures Trading Commission brought its first action invoking a new prohibition under its business conduct standards for swap dealers, while Peregrine Financial Group made news when a US federal court permitted two lawsuits to proceed against one of the banks that held the firm’s customer segregated funds. Meanwhile a new CFTC commissioner invoked Smoot-Hawley to implore cooperation among international regulators regarding the oversight of swaps. Smoot-Hawley? Talk about a great Final Jeopardy™ answer!

As a result, the following matters are covered in this week’s Bridging the Week:

Video Version:

Article Version:

Court Permits Customer and IB Claims to Proceed Against U.S. Bank Over Peregrine Collapse

A US federal court in Illinois authorized two lawsuits arising from the collapse of Peregrine Financial Group to proceed against U.S. Bank, N.A., rejecting requests from the bank to dismiss the proceedings. Peregrine customers brought one lawsuit, while Fintec Group, Inc., a former introducing broker to Peregrine, commenced the other. Both cases were brought as potential class action lawsuits.

Peregrine was a futures commission merchant registered with the Commodity Futures Trading Commission until July 2012 when it filed bankruptcy following the revelation that Russell Wasendorf, Sr., its principal owner and chief executive officer, had committed fraud by using customer funds for his own purposes. Initial estimates were that Peregrine customers’ cash shortfall might exceed US $200 million or more.

U.S. Bank was the principal bank where Peregrine maintained customer funds.

In the customer lawsuit, plaintiffs claimed that U.S. Bank was liable for funds misappropriated by Mr. Wasendorf that had been deposited with it by Peregrine on the basis of a number of legal theories. The court rejected plaintiffs’ claims that U.S. Bank aided and abetted Peregrine’s and Mr. Wasendorf’s own violations, on the grounds that U.S. Bank had no actual knowledge of Mr. Wasendorf’s fraud. The court also rejected a claim of negligence against U.S. Bank because the plaintiffs were not direct customers of the bank, and thus the bank had no duty of care towards them. However, the court allowed plaintiffs’ lawsuit to proceed based on their claims of U.S. Bank’s breach of fiduciary duty, fraud by omission and a violation of an Illinois law dealing with the obligations of fiduciaries.

According to the court, Peregrine established a specially designated customer segregated account at U.S. Bank. However, “[d]espite the fact that the [relevant account] was a customer segregated account, U.S. Bank employees performed numerous transactions out of the [relevant account] for non-customer purposes.” These transactions included transferring substantial funds to personal accounts of Mr. Wasendorf and his wife (including almost US $2.5 million to his wife in connection with the couple’s divorce) and over US $24 million to the account of another company owned by Mr. Wasendorf. The court claimed that Mr. Wasendorf also granted a contractual right of setoff to the Peregrine customer segregated account in connection with guaranties provided to U.S. Bank by Mr. Wasendorf and his wife for a US $6.4 million loan to build a new Peregrine headquarters building. The court claimed that these and other alleged facts are sufficient, at this time, to support plaintiffs’ action:

Although taken individually, [these facts] are not sufficient to establish bad faith, when considered together, they suffice at this state to allow Plaintiffs to move forward with their claims.

Fintec made similar factual claims in its lawsuit, as did the customers. The court dismissed the majority of Fintec’s legal theories. However, the court permitted Fintec’s lawsuit to proceed based on alleged violations of relevant federal law dealing with the bank’s obligations in connection with holding customer funds. The court reasoned that, because U.S. Bank apparently held funds in the customer segregated account that Fintec had deposited with Peregrine to guarantee the trades of its customers, Fintec’s funds were “in connection” with making futures contracts. The court found this nexus sufficient to permit Fintec to proceed on its claims that U.S. Bank violated federal law directly, as well as that it aided and abetted a federal law breach by Peregrine.

(Click here to see the article regarding the CFTC prior actions against Ms. Veraja-Snelling, the former outside Peregrine auditor, and U.S. Bank related to the collapse of Peregrine, "CFTC Sues Peregrine Financial Group External CPA: Says Her Audits Were Not Up To Professional Standards and She Missed Signs of Problems" in the August 26, 2013 edition of what is now known as Between Bridges. Click here to see the article regarding a prior settlement between the Peregrine bankruptcy trustee and JP Morgan Chase related to the bank‘s involvement with Peregrine, “Peregrine Trustee Reaches Settlement with JP Morgan Chase” in the March 31 to April 4 and April 7, 2014 edition of Bridging the Week.)

CFTC Commissioner Giancarlo Invokes Smoot-Hawley to Remind Global Regulators of the Dangers of Uncoordinated Swaps Regulation

New CFTC Commissioner J. Christopher Giancarlo used the occasion of a derivatives industry conference in Geneva, Switzerland to plea for better cooperation among international regulators in implementing over-the-counter derivatives clearing and trading mandates initially proposed at a G-20 summit in Pittsburgh, Pennsylvania in 2009.

Invoking the damaging consequences of the US unilaterally implementing trade protection measures following the US stock market crash of 1929—through passage of the Smoot-Hawley Tariff Act of 1930—Mr. Giancarlo argued against unilateral action by regulators—including the CFTC—that could lead to “[a] trade war over swaps market clearing and execution that will be harmful for the US.” He claimed such a trade war would also hurt Europe.

According to Mr. Giancarlo, Smoot-Hawley was enacted at the time to help the US manufacturing and agricultural sector. However, he claimed, promoters of the law failed to give adequate consideration to the international reaction to unilateral US action:

Smoot-Hawley was interpreted as a declaration of trade war at a critical time in the world economy. Smoot-Hawley made the US a special target of discriminatory trade retaliation from some of the US’ largest and most important trade partners. It led other countries to form preferential trading blocs that discriminated against the United States, diverting world trade and delaying economic recovery on both sides of the Atlantic.

Mr. Giancarlo acknowledged that Smoot-Hawley and international reaction did not cause what ultimately came to be known as the Great Depression, but “it made it worse.”

The new commissioner identified the failure of European regulators to recognize US clearinghouses as “qualifying ” and US imposition of trading rules on non-US execution forums doing business with US persons “contrary to common practice in global markets” as evidence of uncoordinated regulation that has already contributed to global market fragmentation. (If European regulators do not recognize US clearinghouses as qualifying by December 15, European-based banks will face prohibitive capital charges when conducting business through such entities.)

Citing some recent signs of progress between the CFTC and European Commission leadership for “a sound and practical basis for regulatory and supervisory cooperation,” Mr. Giancarlo urged, most immediately, for a resolution of the impasse over the status of US clearinghouses:

I sincerely hope that we can fulfill the important goals that the G-20 set for us in Pittsburgh and avoid falling into a misguided global trade war over regulation of derivative financial products. A global economy that is just starting to show signs of recovering from the “Great Recession” cannot bear the reduction in trade and fragmented financial markets that is a looming possibility.

Barclays Entities Settle With UK FCA Over Client Money Rule Breaches and With US SEC for Investment Advisor Compliance Issues

Two Barclays entities on different sides of the Atlantic Ocean settled regulatory matters resulting in sanctions of over US $75 million.

In one action, Barclays Bank plc settled charges with the UK Financial Conduct Authority that alleged it failed adequately to follow requirements related to the protection of client assets. For this, Barclays agreed to pay a financial penalty of GBP 37,745,000 (US $61.3 million).

In the other action, Barclays Capital Inc. agreed to pay a fine of US $15 million to the US Securities and Exchange Commission and implement certain remedial measures for allegedly failing to maintain an adequate compliance system in connection with its wealth management business.

According to the FCA, from November 1, 2007, through January 24, 2012, Barclays Bank failed to maintain “adequate and effective organizational, control and risk management systems” regarding 95 external accounts where client custody assets were held with sub-custodians outside the Barclays Group, and did not “arrange adequate protection for, maintain its own books and records and perform its own reconciliations” related to approximately GBP 16.5 billion (US $26.8 billion) of client custody assets for which it was responsible.

FCA made clear that Barclays Bank’s failings were solely within its investment banking division. No other bank customers or operations were impacted.

FCA noted that, although Barclays Bank self-reported its failings, it did not detect its issues for over three years, and it took approximately eight months for the bank to identify the number of accounts in breach of requirements. FCA acknowledged, however, that no customers were harmed as a result of the bank’s issues and that the bank did not act “deliberately or recklessly.”

Separately, the SEC found that Barclays Capital did not adequately enhance the compliance system of its wealth management business after it acquired the private investment management business of Lehman Brothers in 2008. The SEC also claimed that the firm did not put in place adequate policies and procedures to prevent violations of relevant law and to keep certain required books and records.

Among other things, said the SEC, Barclays Capital engaged in certain principal transactions from January 2009 to December 2011 without making written disclosures and obtaining client consent, as required by law; charged commissions and fees and earned revenue from September 2008 through December 2011 that were not in accordance with client disclosures; and did not ensure that client funds and securities over which it had custody were subject to surprise examinations by an independent public account, as required by an SEC rule.

In agreeing to the settlement, the SEC acknowledged Barclays Capital’s cooperation and the prompt remedial actions it took after learning of its issues, as well as the reimbursement to customers of approximately US $3.8 million, including interest.

In addition to paying a fine, Barclays Capital agreed to retain an independent compliance consultant to review discrete aspects of the firm’s advisory business and issue recommendations, which the firm has committed to adopt unless unreasonable.

And briefly:

Compliance Weeds: Reports of exchange disciplinary actions provide an excellent source of material to include in internal training of staff as they address a diverse set of day-to-day requirements and topics relevant to a number of internal departments (for example: sales, operations, information technology). Most regulatory organizations provide the ability to receive notices of these actions automatically (for example, click here for link to subscribe to CME Group advisories, and here for the link to subscribe to ICE Futures U.S. advisories).

And even more briefly:

For more information, see:

Barclays Entities Settle With UK FCA Over Client Money Rule Breaches and With US SEC for Investment Advisor Compliance Issues:

See also, Barclays’ Response to FCA Settlement:

http://www.newsroom.barclays.com/content/default.aspx?NewsAreaID=2

BIS Reports on Collateral Management:

http://www.bis.org/cpmi/publ/d119.pdf?utm_source=FIA+Weekly+Briefing+-+09%2F26%2F14+&utm_campaign=FIA+WeeklyBriefing_0926&utm_medium=email

CFTC Commissioner Giancarlo Invokes Smoot-Hawley to Remind Global Regulators of the Dangers of Uncoordinated Swaps Regulation:

http://www.cftc.gov/PressRoom/SpeechesTestimony/opagiancarlos-1

CFTC Publishes Text of Proposed Swaps Margin Rules and Final Rule Related to Utility Operations-Related Swaps:

CFTC Sues Trader for Fraud and Unauthorized Swap Trades:

http://www.cftc.gov/ucm/groups/public/@lrenforcementactions/documents/legalpleading/enfevanscomplaint092414.pdf

Court Permits Customer and IB Claims to Proceed Against U.S. Bank Over Peregrine Collapse:

EUREX to Introduce New Margining System—Prisma:

https://www.eurexclearing.com/blob/clearing-en/51618-156326/1084070/2/data/ec14136e.pdf

Father and Son Sanctioned by CFTC for Position Limit Violations:

http://www.cftc.gov/ucm/groups/public/@lrenforcementactions/documents/legalpleading/enfthrasherorder092414.pdf

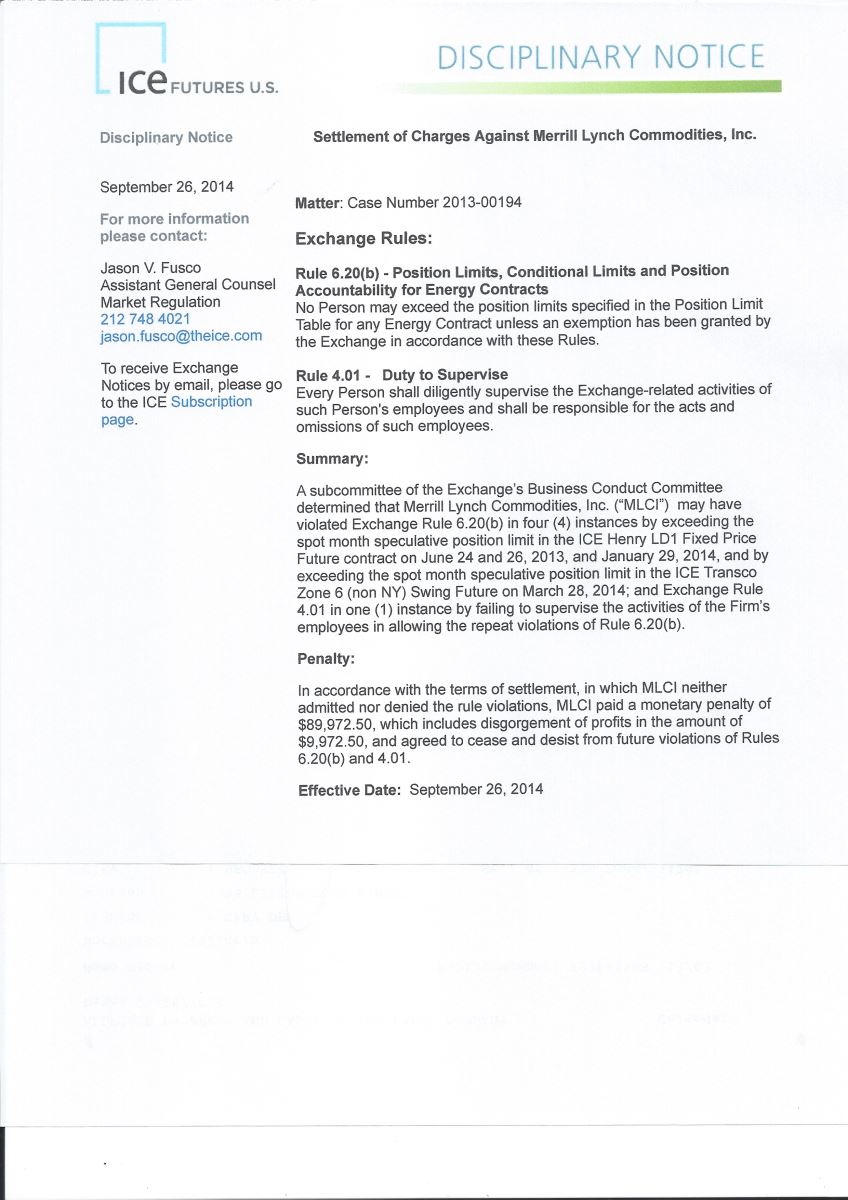

Important Reminders Resonate From Recent CME Group and ICE Futures U.S. Disciplinary Actions:

LME Launches LME Clear:

https://www.lme.com/news-and-events/press-releases/press-releases/2014/09/lme-clear-announces-successful-launch/

October 9 CFTC Global Markets Committee to Address NDFs and Bitcoins:

http://www.cftc.gov/PressRoom/PressReleases/pr7010-14

Ontario Securities Commission Issues Guidance Regarding Unsolicited Trade and Hedger Exemption for Unregistered Foreign Dealers Facilitating Futures Transactions With Ontario-Based Customers:

http://www.osc.gov.on.ca/documents/en/Securities-Category3/sn_20140918_33-744_availability-registration-exemptions-foreign.pdf

See also

Shanghai Gold Exchange Opens to International Clients:

http://www.en.sge.com.cn/news-announcement/announcement/520051.shtml

The Other Shoe Drops: After Previously Fining FirstRand Bank for Unlawful Pre-Execution Discussions, CFTC Now Fines the Counterparty, Absa Bank:

http://www.cftc.gov/ucm/groups/public/@lrenforcementactions/documents/legalpleading/enfabsaorder092514.pdf

See also: CFTC v. FirstRand Bank:

http://www.cftc.gov/ucm/groups/public/@lrenforcementactions/documents/legalpleading/enffirstrandorder082714.pdf

The information in this article is for informational purposes only and is derived from sources believed to be reliable as of September 27, 2014. No representation or warranty is made regarding the accuracy of any statement or information in this article. Also, the information in this article is not intended as a substitute for legal counsel, and is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. The impact of the law for any particular situation depends on a variety of factors; therefore, readers of this article should not act upon any information in the article without seeking professional legal counsel. Katten Muchin Rosenman LLP and/or Gary DeWaal may represent one or more entities mentioned in this article.

Quotations attributable to speeches are from published remarks and may not reflect statements actually made.

Gary DeWaal is currently Special Counsel with Katten Muchin Rosenman LLP in its New York office focusing on financial services regulatory matters. He provides advisory services and assists with investigations and litigation.

|

Social Media: |

May 03, 2020

April 12, 2020

March 29, 2020

Katten is a firm of first choice for clients seeking sophisticated, high-value legal services in the United States and abroad.

Our nationally recognized practices include corporate, financial services, litigation, real estate, environmental, commercial finance, insolvency and restructuring, intellectual property, and trusts and estates.

Our approximately 650 attorneys serve public and private companies, including nearly half of the Fortune 100, as well as a number of government and nonprofit organizations and individuals.

We provide full-service legal advice from locations across the United States and in London and Shanghai.

Gary DeWaal

Katten Muchin Rosenman LLP

575 Madison Avenue

New York, NY 10022-2585

+1.212.940.6558

{kind=link}

Bridging the Week by Gary DeWaal: September 22 to 26 and 29, 2014 (Peregrine; Smoot-Hawley; Unauthorized Swap Trades; Ontario Exemptions; Father and Son Sanctioned Together)

Jump to: Bitcoin Ecosystem